UK cross-border B2B payments: the £30T opportunity most platforms are still under-serving

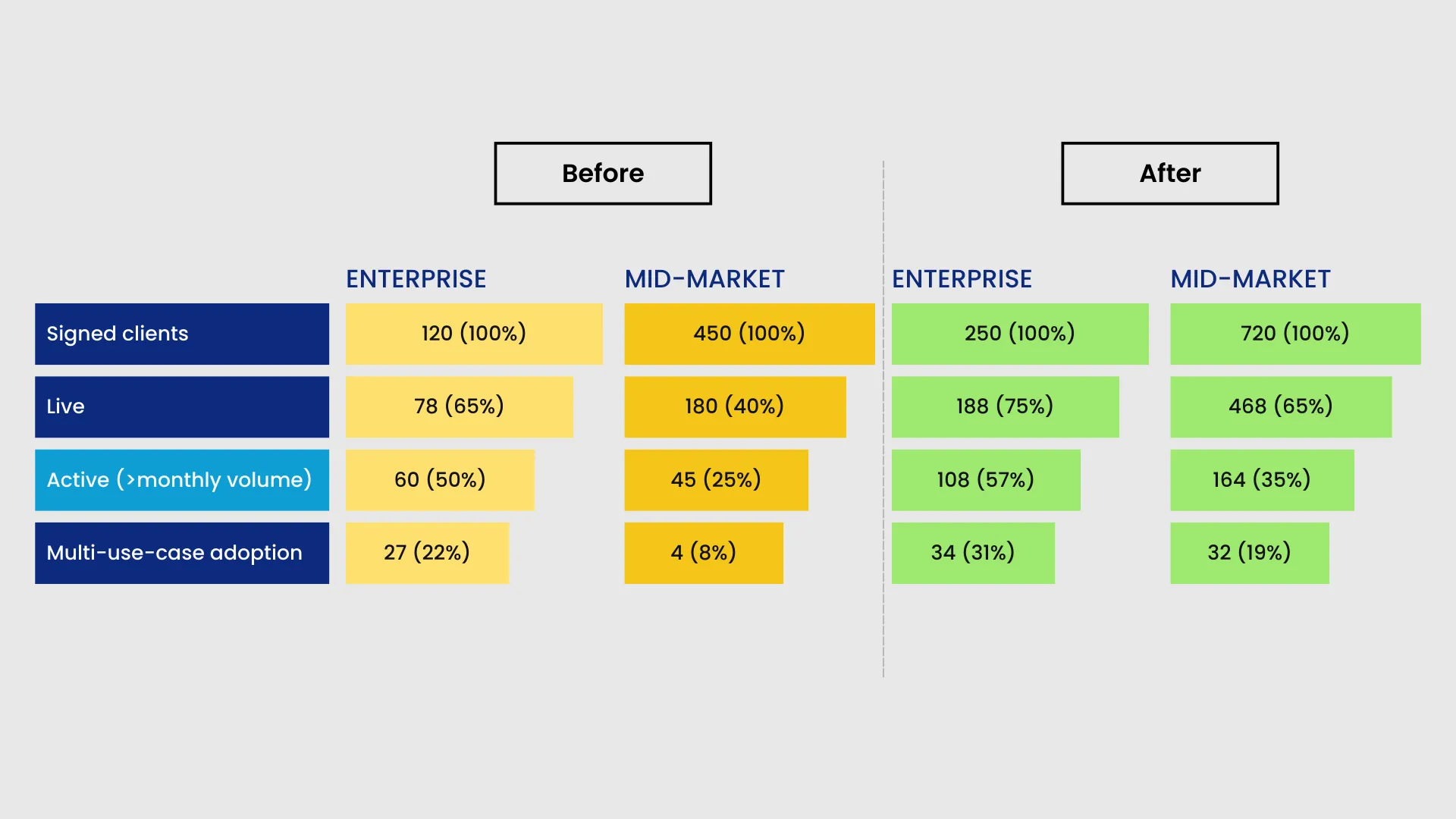

SMB and platform-driven cross-border payments are growing at 15–20% CAGR — yet the majority of UK fintechs process less than 30% of their potential corridor volume through real-time rails. The gap between contract signature and active TPV remains the single largest source of unrealised revenue across our UK client base. This quarter, we're focused on closing it.

Three structural shifts are reshaping the landscape: the acceleration of embedded cross-border settlement in vertical SaaS platforms, the rapid normalisation of instant gig/EWA payouts as a retention tool, and growing regulatory pressure on settlement latency in the UK–South Asia and UK–West Africa corridors. Clients who activate these use cases before Q2 will benefit from first-mover volume concentration in routes where network effects compound.

New corridor routes now live — what this means for your business

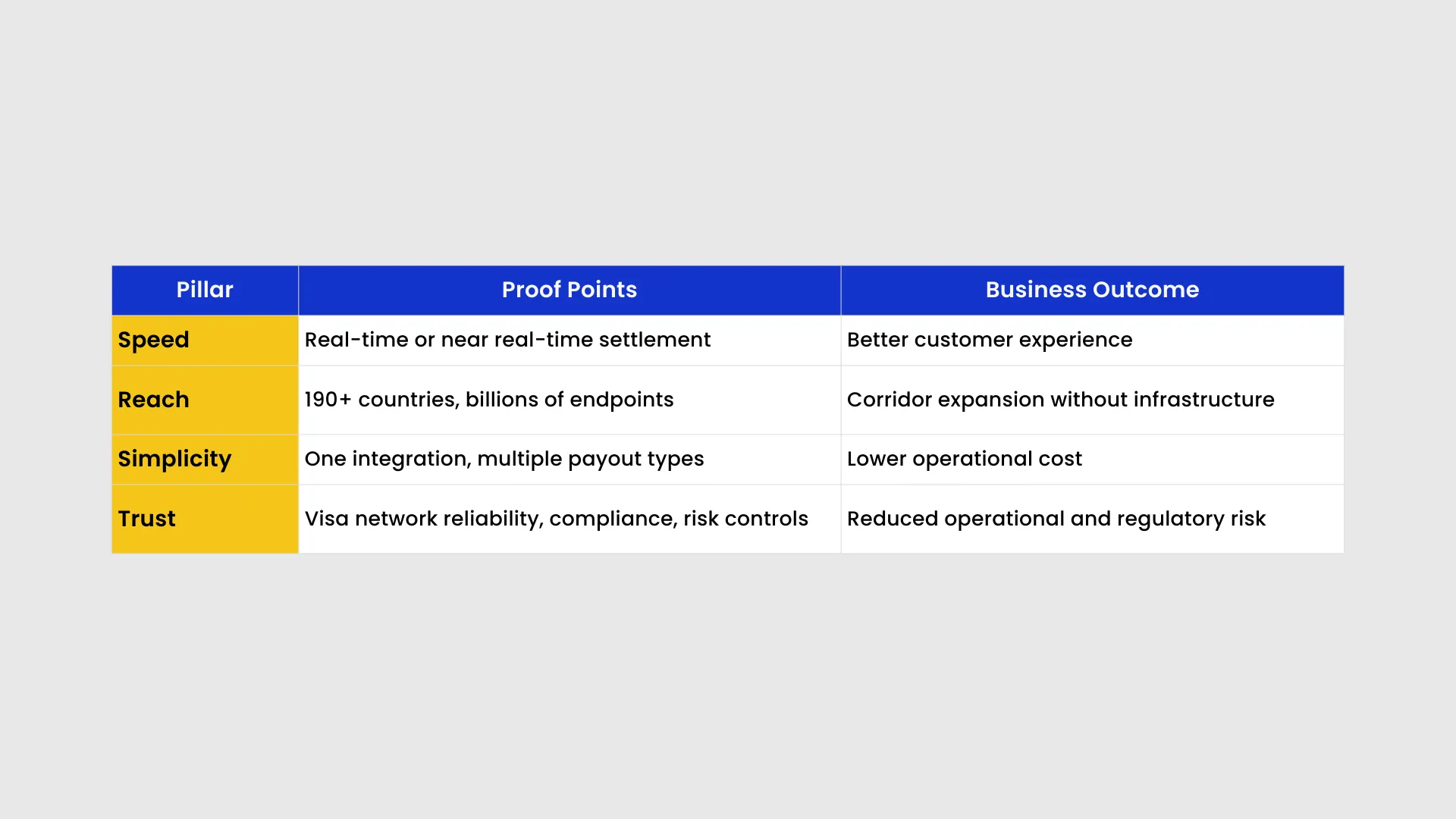

Four high-demand corridors have expanded settlement coverage this quarter. If your customers transact in any of these routes, you can now offer real-time or same-day delivery without infrastructure build.

To see which of these corridors apply to your existing integration, contact your Client Success lead or request a personalised Corridor Opportunity Analysis.

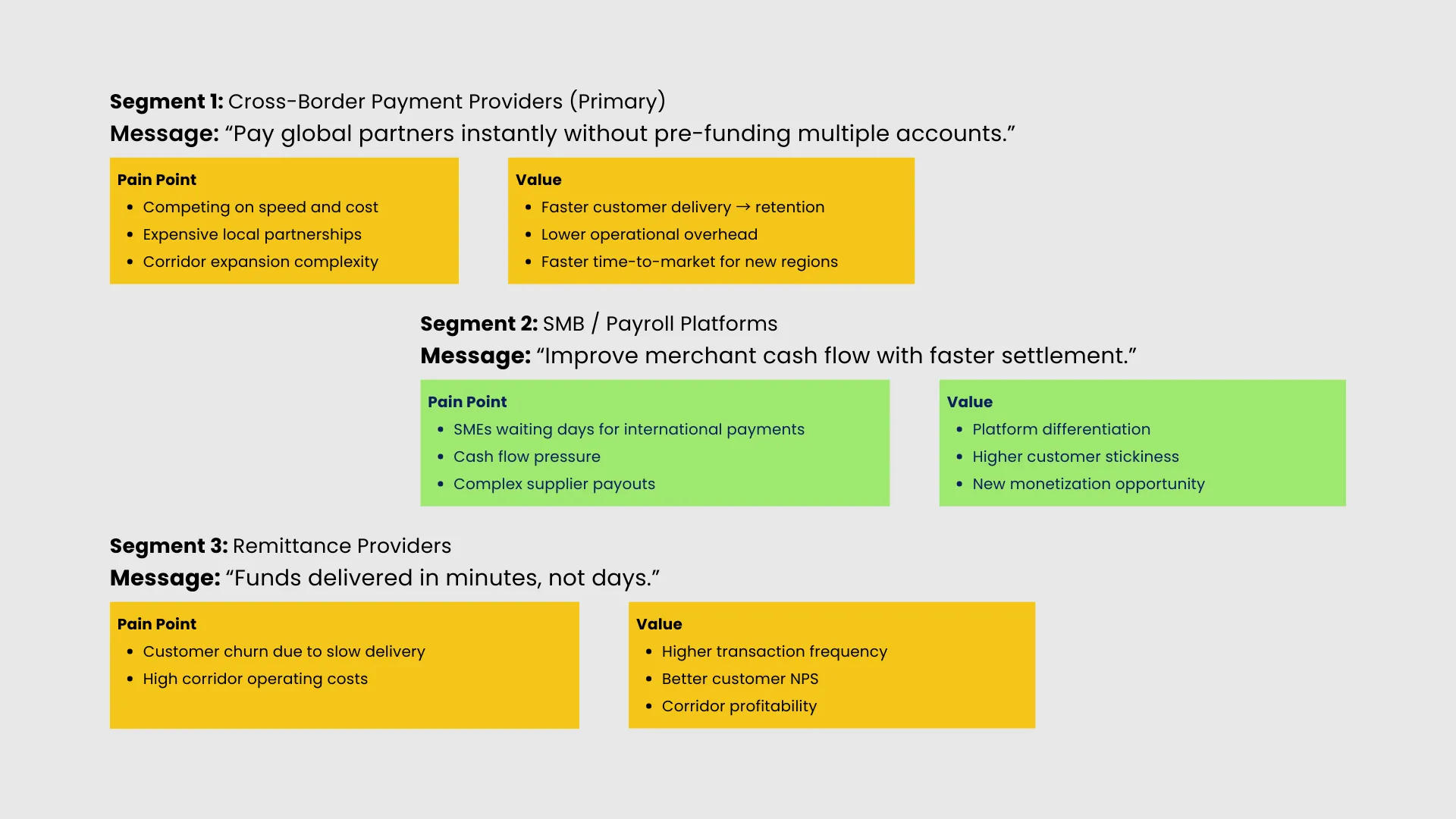

Gig & earned wage access: the fastest-growing payout use case in UK

Platforms that migrated from weekly batch payroll to real-time EWA disbursements via Visa Direct reported measurable gains in worker retention and platform engagement. This is no longer a differentiator — it's becoming the base expectation for UK gig economy platforms.

"Moving to instant payouts through Visa Direct reduced our worker churn by double digits in the first quarter. The integration took six weeks."

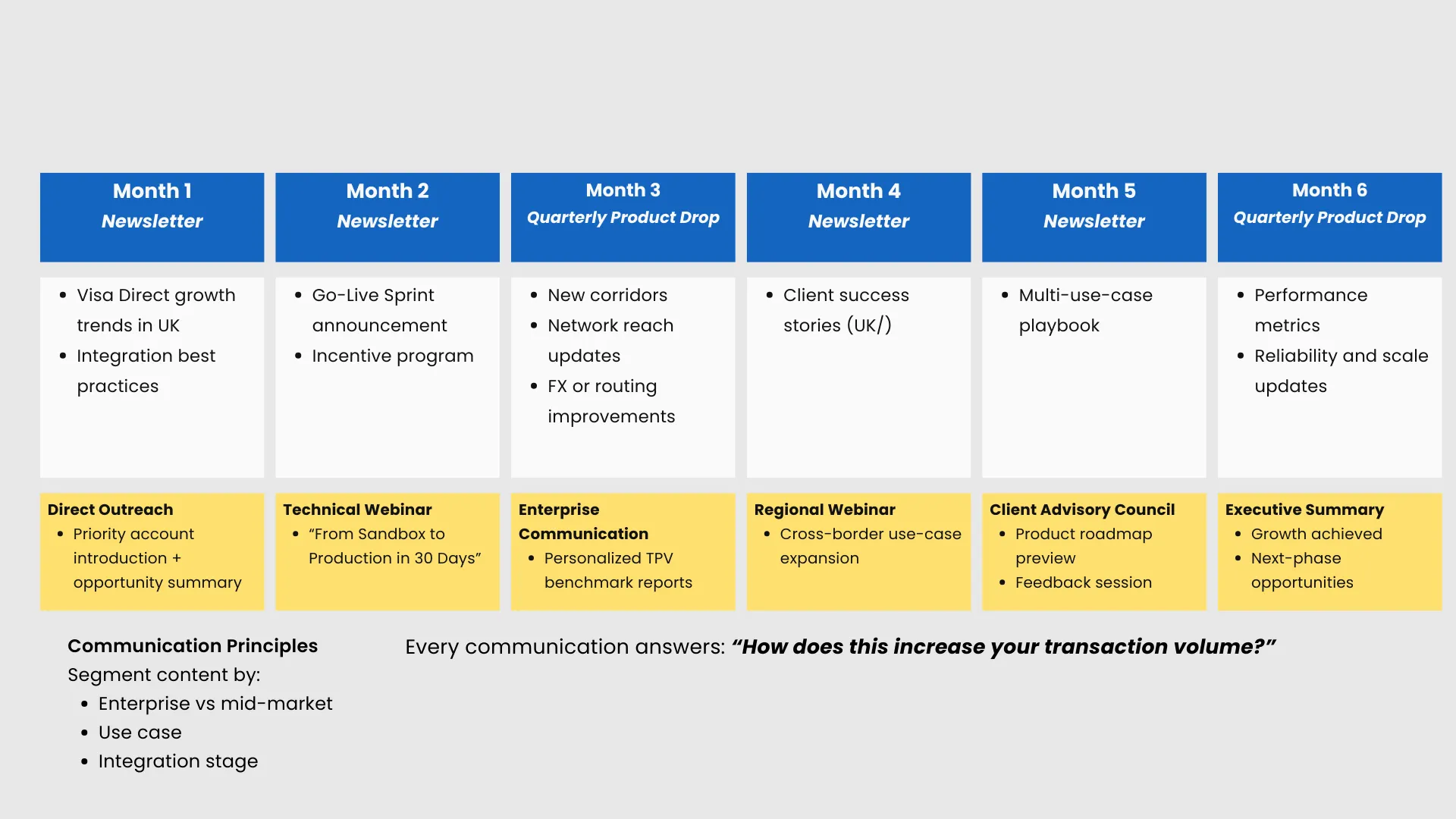

What shipped this quarter — and what's coming

Updates directly relevant to UK client integrations:

Technical webinar & executive briefings

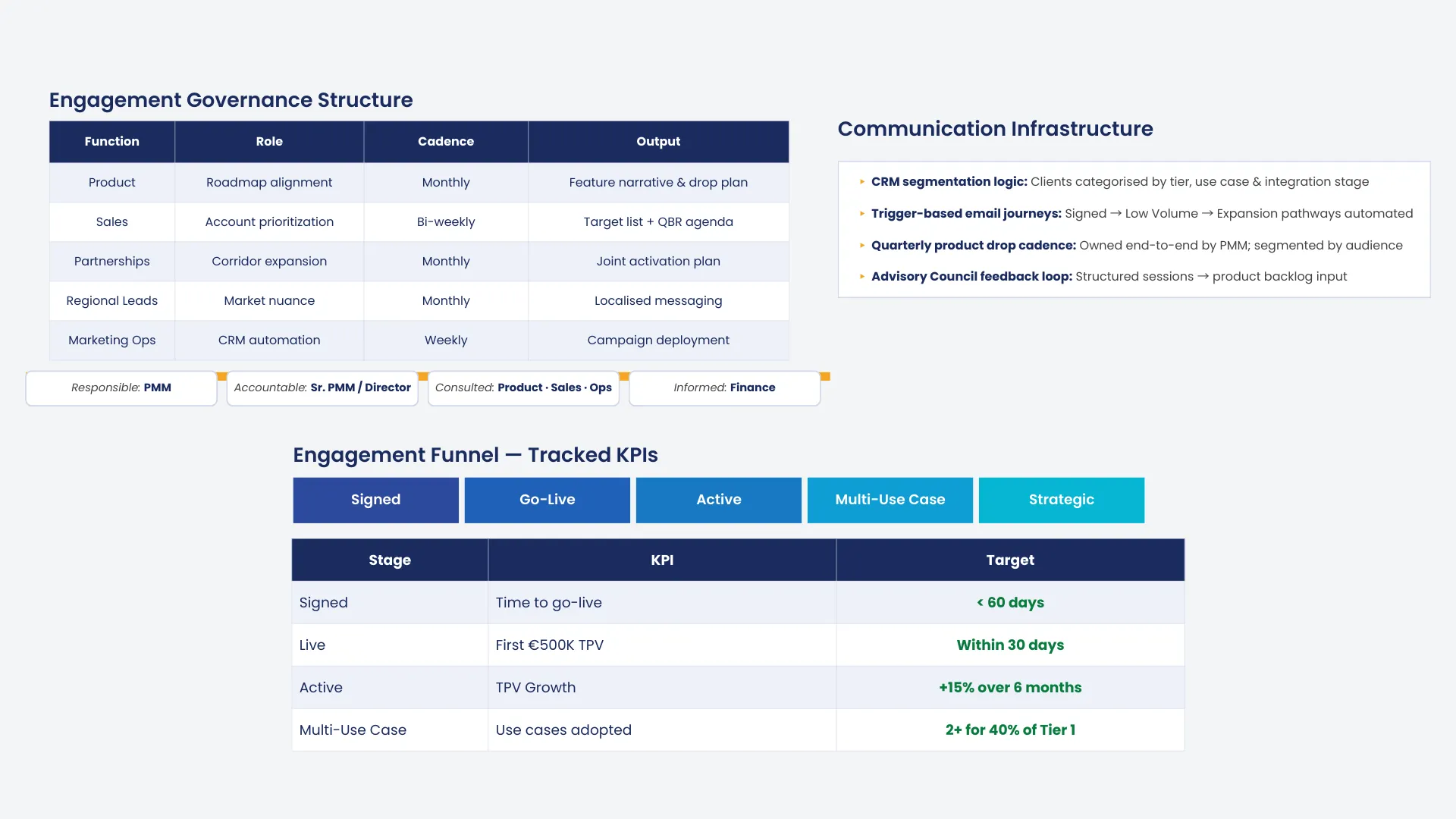

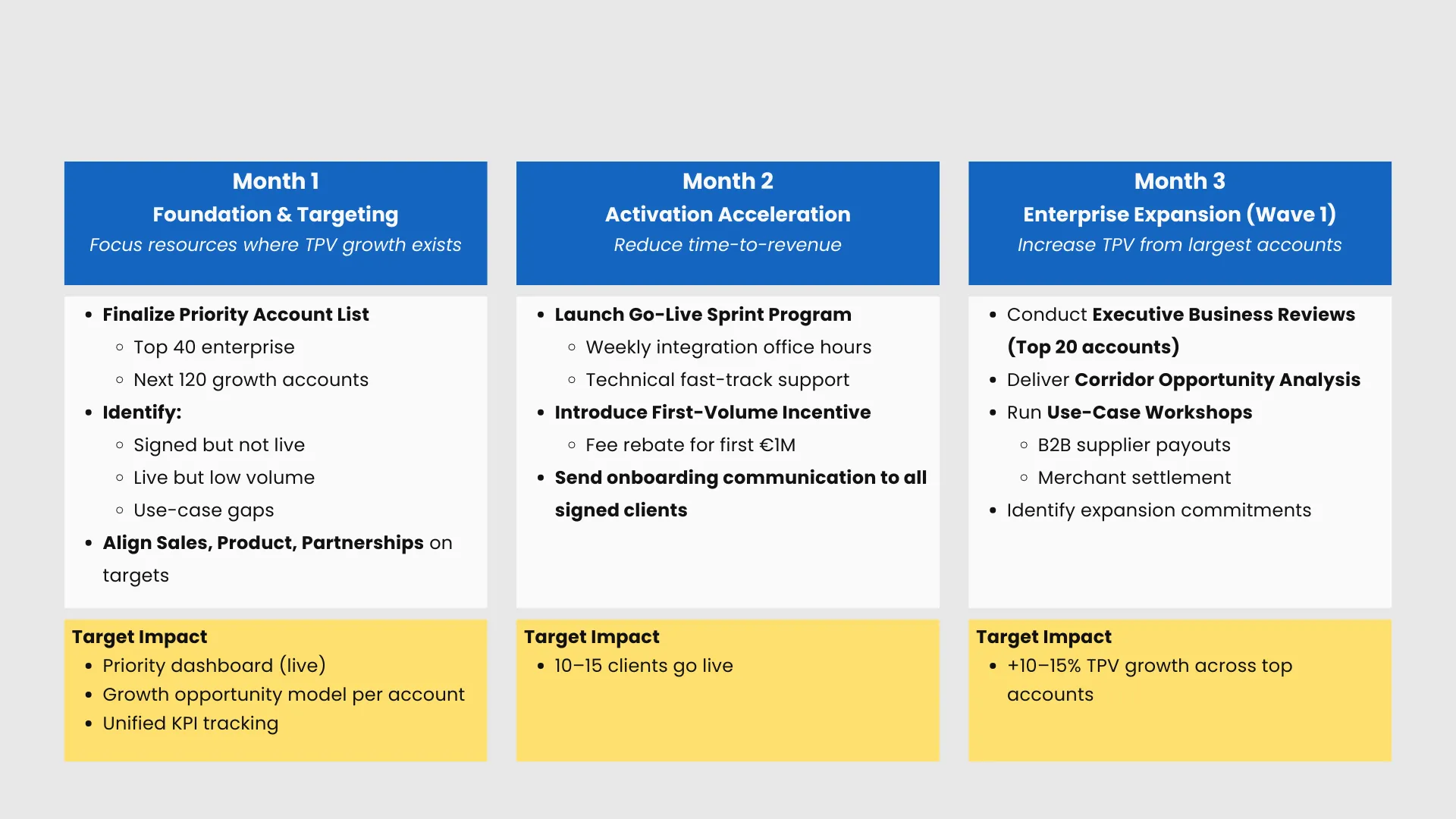

Your next TPV milestone starts with one conversation

Whether you're signed but not yet live, active but under-utilising corridors, or looking to add a second use case — your Client Success Manager has a tailored playbook ready.